Discover valuable insights from multifamily broker Joe LaFleur

100Units recently hosted our Connect and Invest event for multifamily owners featuring our founder and multifamily investment advisor, Joe LaFleur. He shared tips and in-depth insights on multifamily financing and the latest market trends of 2023.

During our virtual event, Joe discussed how to make your offer stand out to a seller and achieve your goal of buying more properties.

Join us as we learn from Joe and his deep understanding of multifamily financing and current market trends. You can find the link to watch the virtual event in full below.

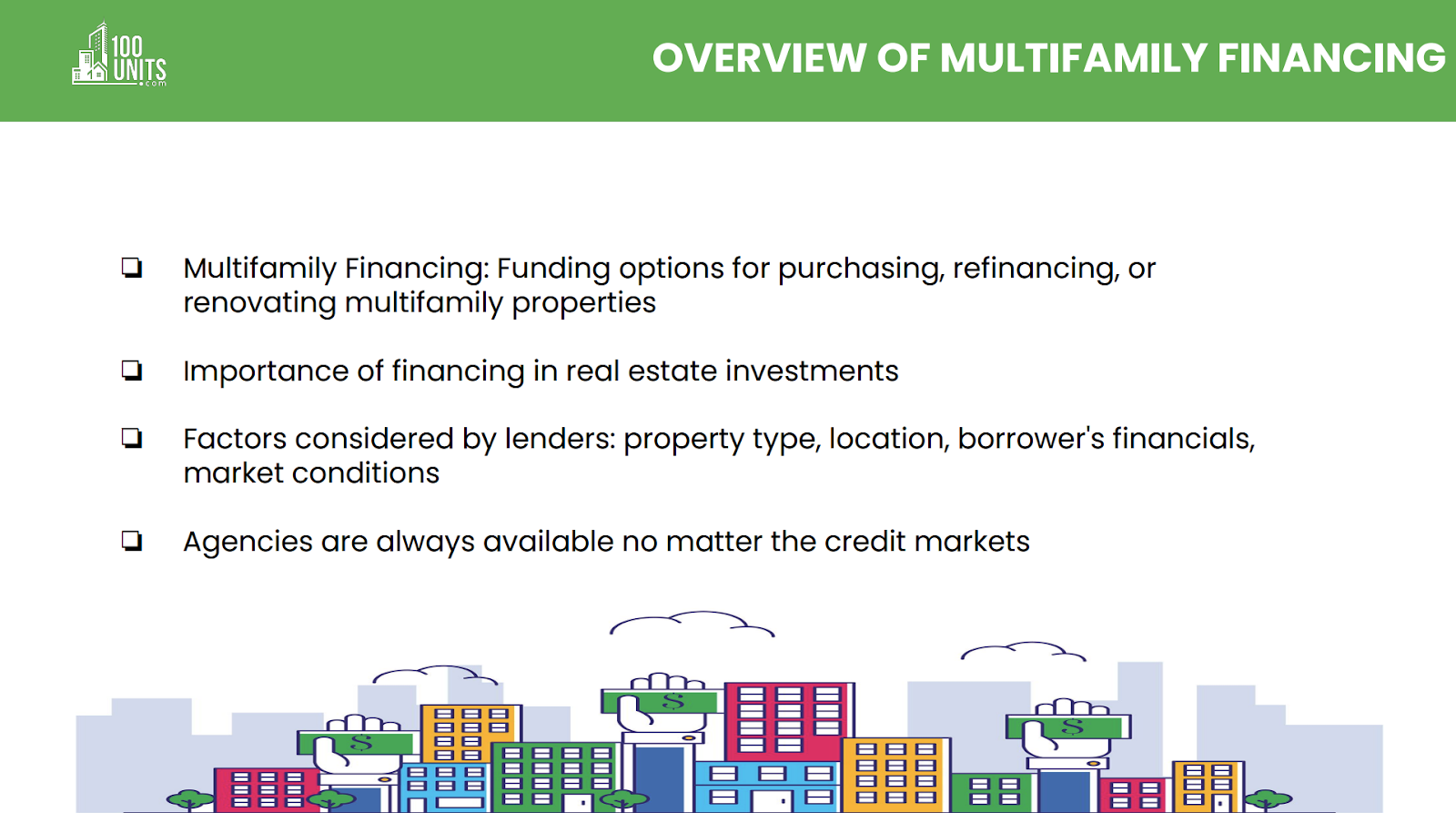

What is the purpose of multifamily financing?

A clear idea of where the current market stands can help you determine how to approach your finances. Leveraging your investment dollars to maximize the property you’re purchasing can build your portfolio faster.

Joe LaFleur shares that “one of the major keys regarding real estate is your ability to leverage your investment dollar. One of the major differences that you’re going to see between multifamily assets and all of the other major food groups, office, industrial, and retail, is multifamily is the only one that has the agencies, which are government-sponsored enterprises that are at all times a backstop to lending and adding liquidity into the market.”

Where should you look for your multifamily financing?

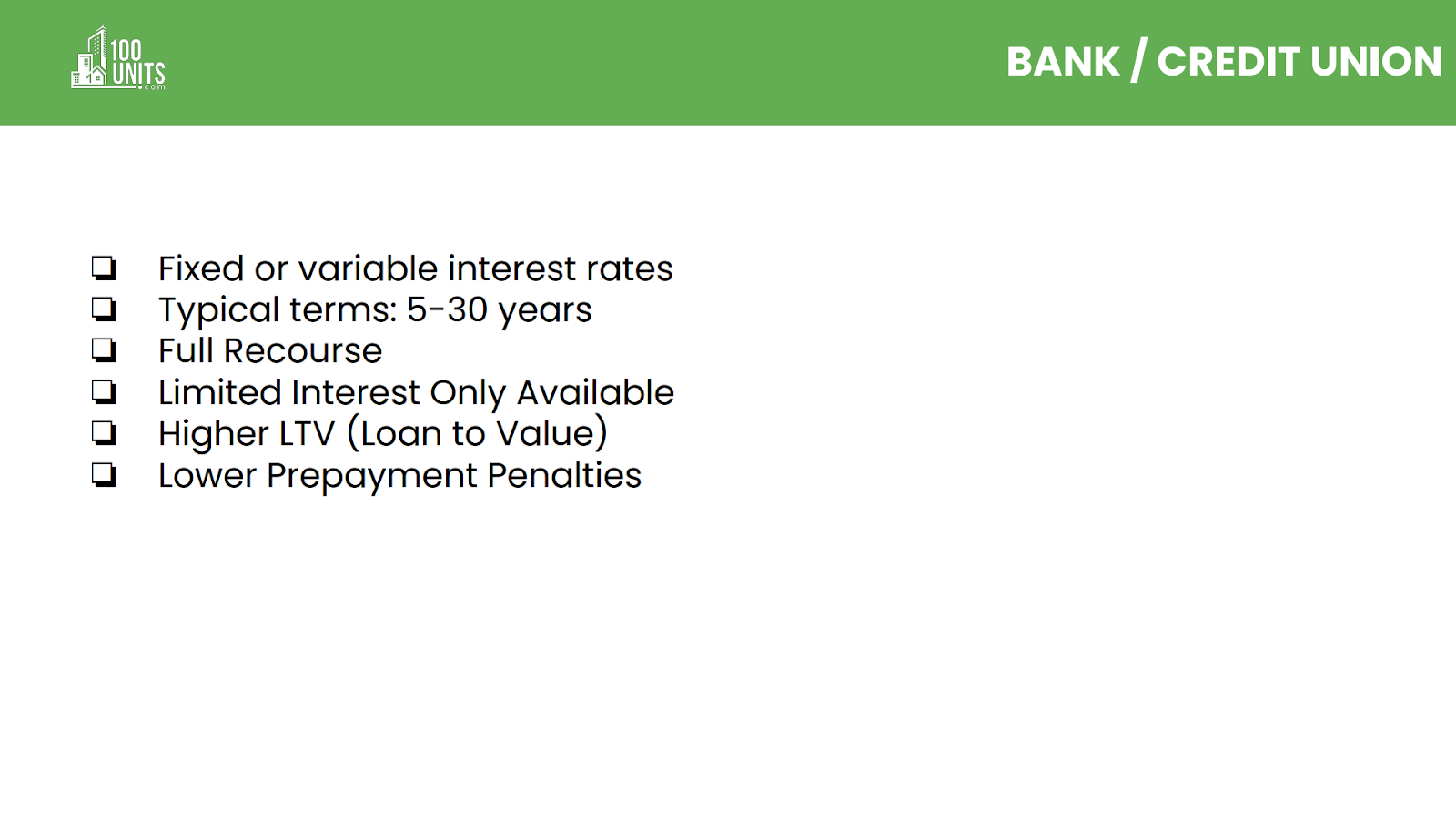

The vast majority across investment real estate has shown that 65% of most deals under $5 million are done with banks and credit unions.

Joe’s tip: “A good mortgage broker has relationships not just with one or two banks but 40 of them because each month, each quarter, those buckets are changing for each one of those institutions. So it’s very important to know which ones are active today and offering the best terms for you and which ones are being more conservative or offering not quite as good terms.”

“Some credit unions or banks will give you fully amortizing 30-year mortgages. Across the board, there are going to be recourse loans. Limited interest only. On occasion, you’ll get 12, maybe 18, 24 months of interest only if you are buying a value-added property, depending on the bank or the credit union. Their loan-to-value is typically higher than you’ll get from the agencies, but it is a recourse loan. One of the advantages that they bring to the table is typically their prepayment penalty. Yield maintenance is going to be smaller than most agencies or CMBS because the money is theirs, and it’s going to be returned, and they’re going to be redeploying that capital,” explains Joe.

“If you are looking for something where your intention is to refinance or sell the property in under three years, banks are typically a good option because of the lower prepayment penalties they offer,” concluded Joe.

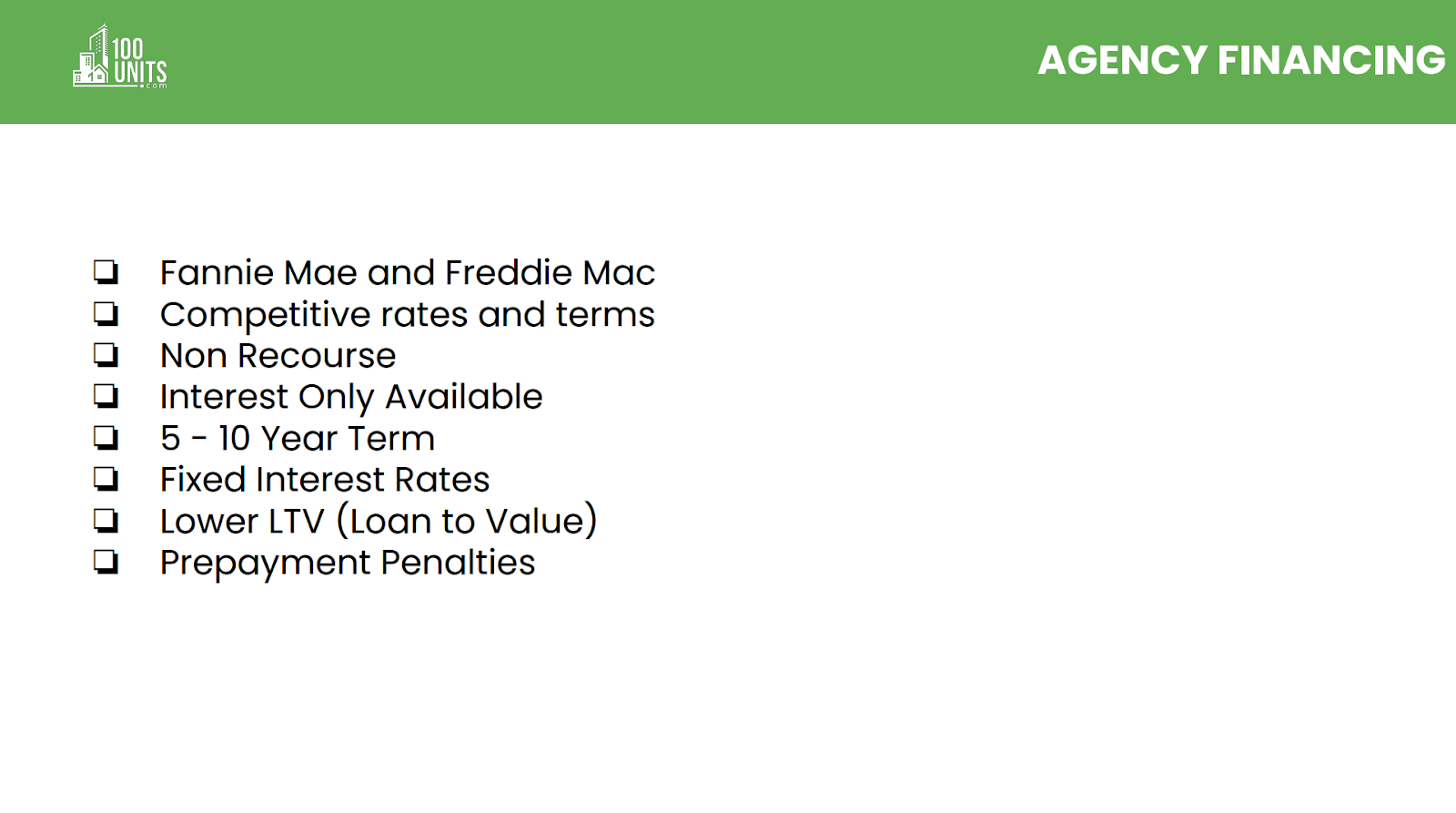

Agency financing

Agencies, similarly to credit unions, offer competitive financing options. Top agencies like Fannie Mae and Freddie Mac provide non-recourse loans, and specifically, Fannie Mae will offer full-term interest-only loans. If you were to pick a 10-year loan, you can get ten years of full interest-only, full-term IO for ten years.

“It’s important to pay attention to what is constrained by debt service coverage ratio, which means they will be a lower loan to value. Your proceeds coming out of this loan will typically be lower than most of your other alternatives. They will also have significant prepayment or yield maintenance penalties where if you try to pay that 10-year loan off early, it can be a significant amount of money. How they work on their backend is they give out 1,000 loans, bundle them all together, securitize those, and then sell them out with Fannie Mae or Freddie Mac as the backstop behind them guaranteeing the loans. But that means they don’t really want to get paid off ahead of time, so their prepayment or yield maintenance penalties can be significant,” explains Joe.

Related resource:

Our ultimate guide to expertly financing your multifamily property

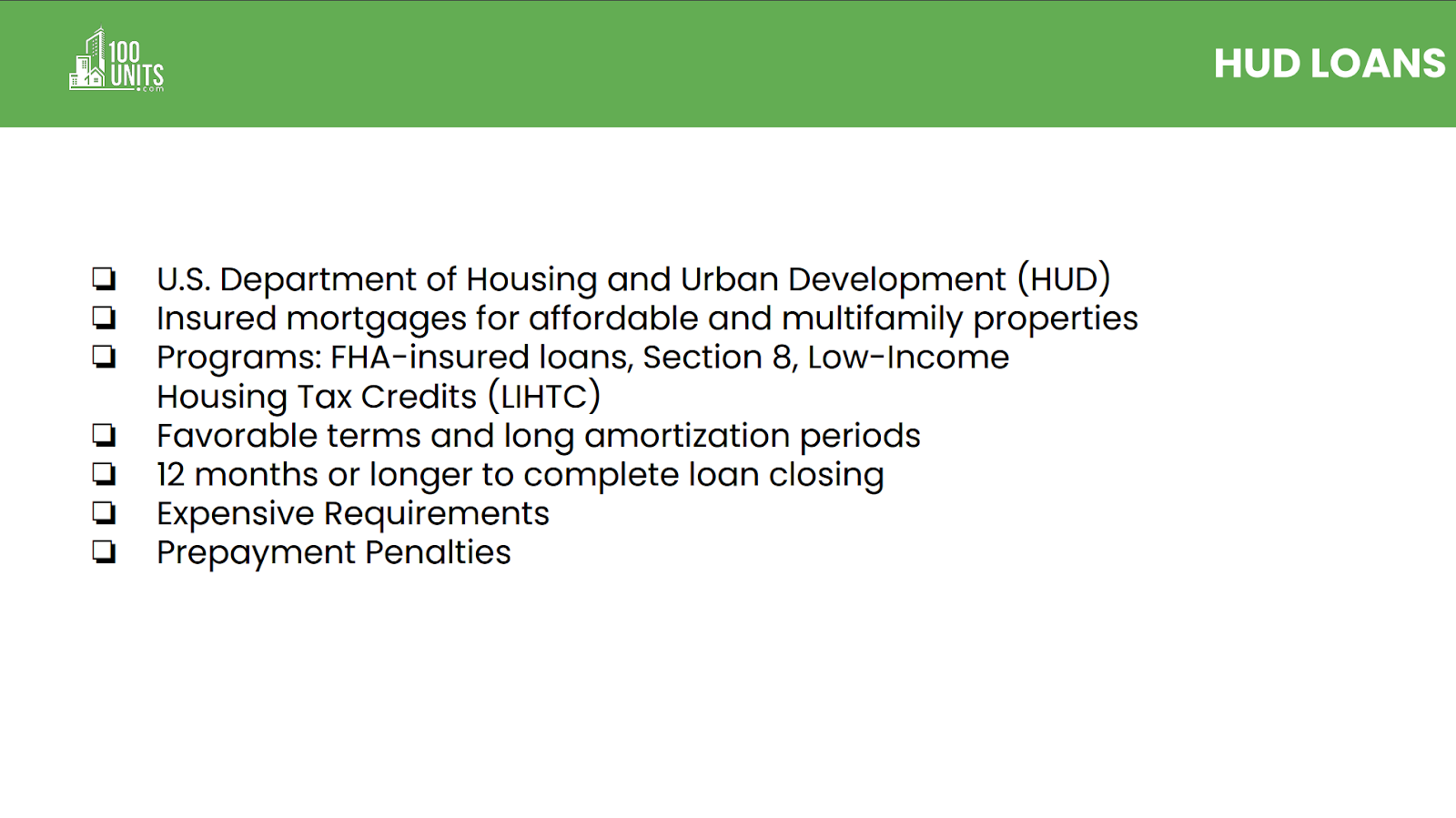

HUD loans

HUD loans are not typically something you will not see on a purchase. This type of loan takes time and requires a deep understanding of how it works. It’s best to seek a HUD loan specialist to ensure your interest rates and financing options are favorable.

“The big caveat with HUD loans is the amount of time the loan takes. The vast majority of anything we’ve been involved in with HUD has been cash-out refinances after two or three years of stabilization. The reason is that the loan takes over a year to get done. If you are going to go down the road of getting a HUD loan, I strongly recommend you find a HUD loan specialist. I would get someone who only does HUD because they have extremely extensive requirements, and there is very little flexibility in those, and if you miss one thing on there, you’re starting all over again,” shares Joe.

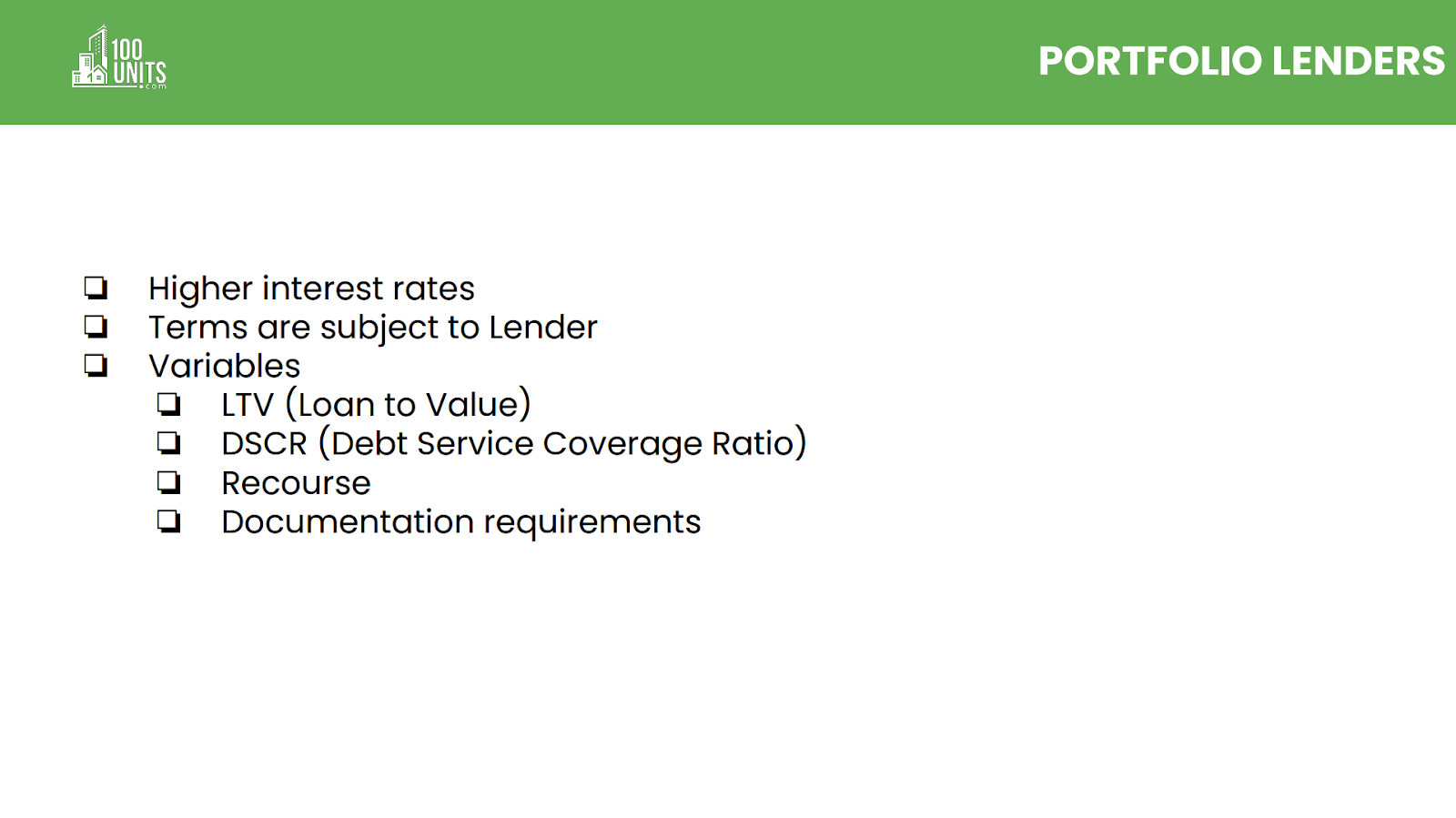

Portfolio lenders

A portfolio lender is someone who places their equity out into the market at their discretion. They get to pick the terms and interest rates that work best for them. Their interest rate will be significantly high, about a 2% increase above a bank or credit union, and well above Fannie Mae and Freddie Mac.

“The reason they are charging that additional interest is they’re going to give the borrower flexibility as far as terms. So the loan to value, they have the right, it’s their equity so that they can take it all the way up to 80%, some more. The debt coverage ratio, they could even go down to a 1.0 debt coverage because it’s their money, so they can set the terms however they want,” details Joe.

“If you need flexibility in your loan, you’ll pay a higher interest rate. But there is a lot of flexibility in the space of portfolio lenders, and these were nowhere near as active as they are today, a decade ago. This space has gotten very active, and it’s something that plenty of borrowers are overlooking when they need that kind of flexibility in their loan,” concluded Joe.

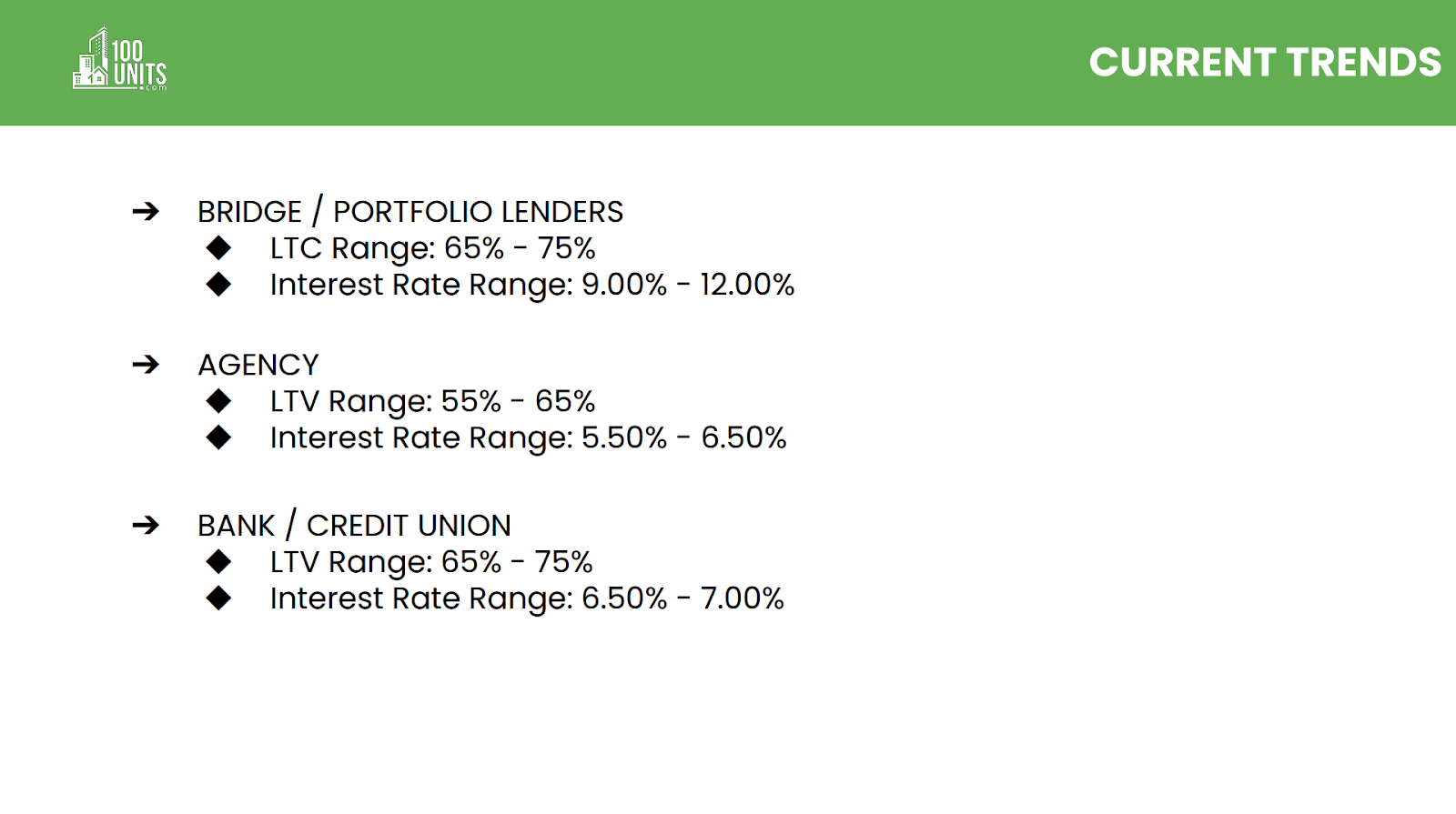

What are the current trends?

While we know trends can fluctuate, examining the current trends is essential to help prepare your finances. Joe shared his take on today’s trends and how these trends can directly affect the condition of your financial state:

“Our current trends, the things that we’re seeing out in the marketplace right now that are between all of the spaces, to give an idea of bridge loans or portfolio lenders, you’re in the 65-70% LTV and 9-12% interest rate. And again, if you notice, there’s a wide range, and the LTV can move up or down depending on the exact lender—the same thing with the interest rates. Typically, you won’t get much below 9%, maybe 8% for bridge or portfolio lenders. Still, they are incredibly flexible when it comes to documentation terms, debt coverage ratio, and loan-to-value. Their range is very wide because it’s their money, and they can do whatever terms they deem necessary to make a deal happen.”

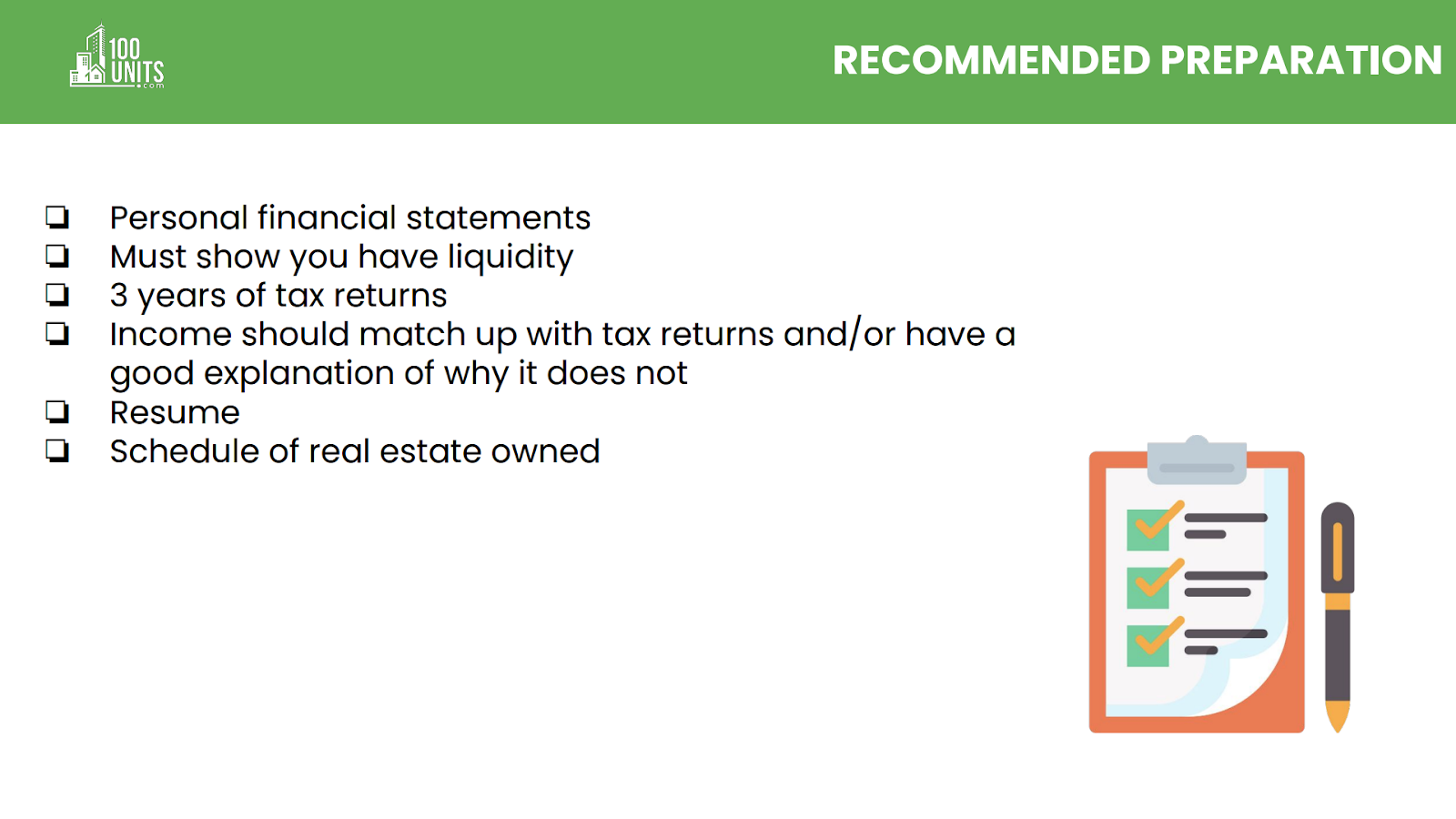

How do you prepare your finances, and what do we recommend?

Whether you are new to multifamily financing or just getting started, we’ve provided our best practices and insights acquired from over a decade of experience within the business. Joe shares his tips on preparing your assets:

“One of the keys that I’ve seen over and over is they have their liquid assets specifically separated. That way, it’s very easy for the lender and the lender’s underwriter without having to dig through financial statements to determine what’s a liquid asset and what’s not. They have it separated with clearly stated liquid assets where they can see the total. Because that’s one of their check-boxes, that’s very important for them to see. Typically, they will ask for three years of tax returns, so having those ready to go is important.”

“If the income that you’re showing on personal financial statements or from some of your businesses is vastly different from the income shown on the tax return, say you’d bought several properties, done cost segregations on each of them, so you had greatly reduced the income that you’re showing on your tax return. It’s important to state that clearly, explain it, and give it to the lender beforehand. This will save a lot of headaches,” shares Joe.

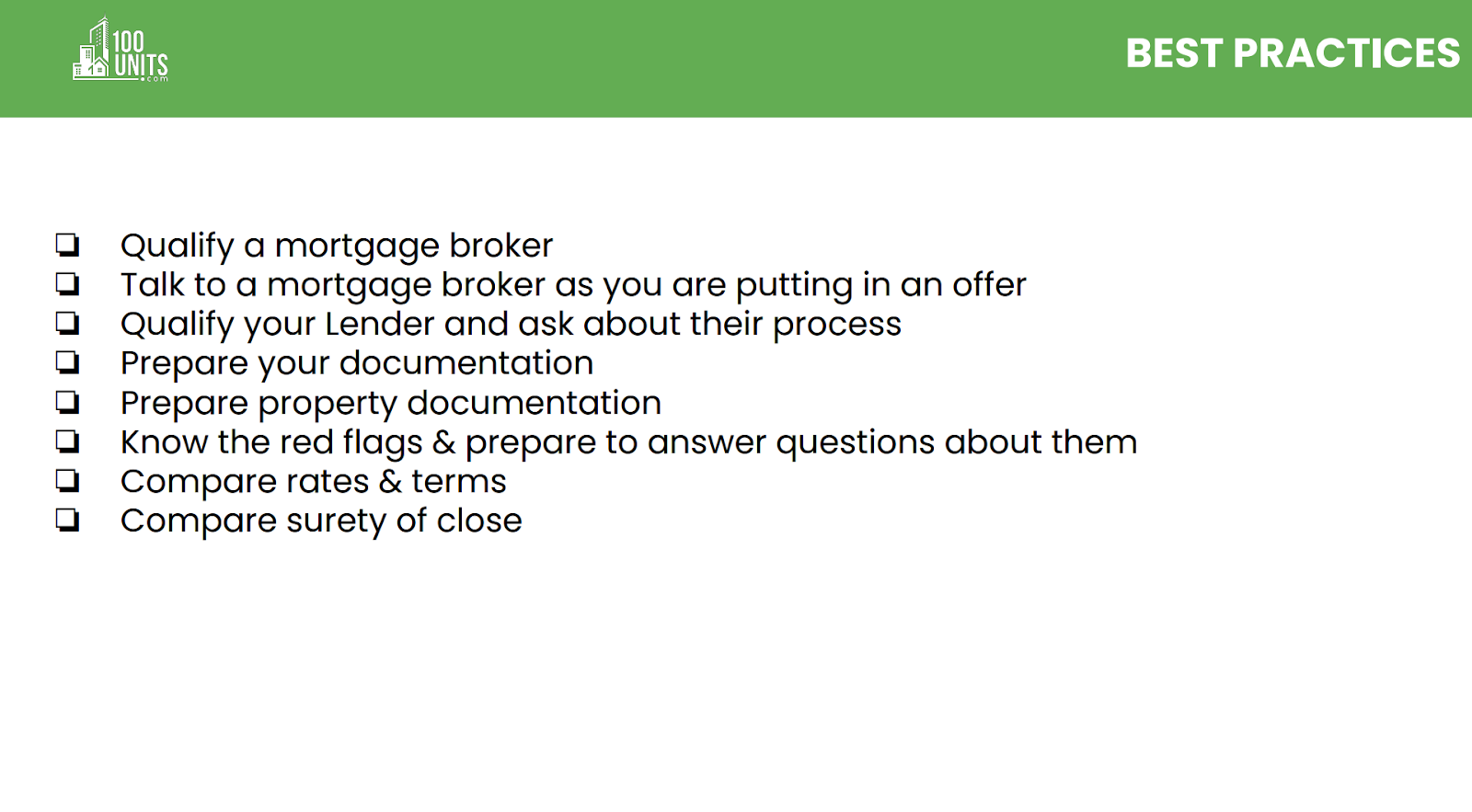

Best practices

Joe details his best practices and gives an overview of how to utilize mortgage brokers and lenders to execute the ideal loan and property that suits your needs.

“Across the board, the people we see execute the best typically use a mortgage broker. They have so many connections and can connect you across a wide spectrum of lenders that you may be unable to talk to or even know they’re out there lending right now. The vast majority of the people I deal with use a good mortgage broker.”

“The surety of close is an art, and it’s something that you’ll become better at over time, but don’t just discount it by going after the cheapest interest rate and the best terms. A surety of close where you can execute that loan can be worth a significant amount of money. And I’ve seen some people make a mistake where they just went after the lowest price and terms, costing them significantly right at the closing table. So it’s something to be very aware of,” Joe concluded.

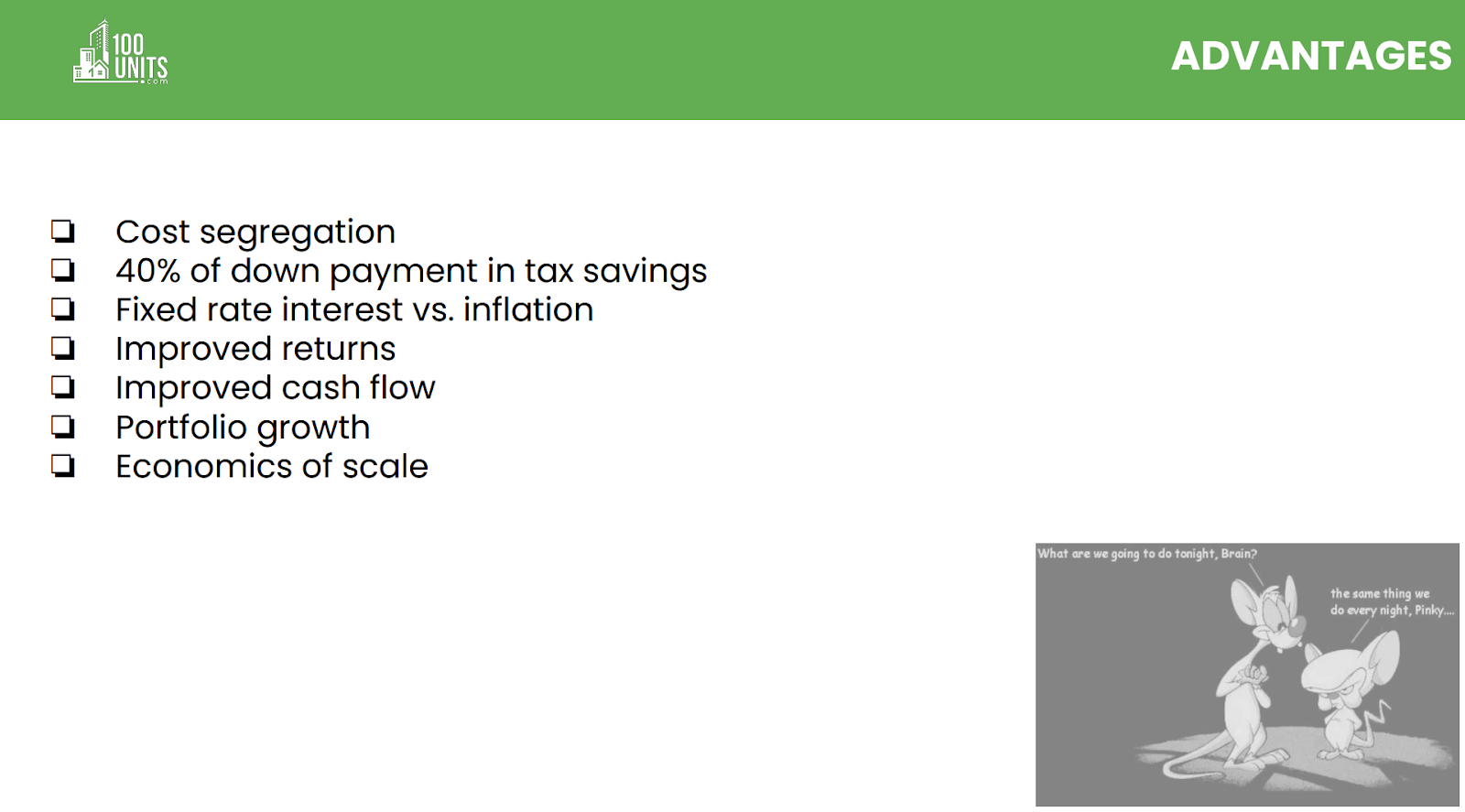

Advantages of using leverage

The benefit of using leverage for multifamily financing is to grow your portfolio faster. If you’re borrowing money, it’s essential to evaluate the current state of inflation to determine what’s best for your financing options.

“If you are in a situation where you’re looking for tax advantages, cost segregation, by using leverage, you’re going to be able to get back, typically in tax savings, 40% of the down payment amount that you’ve used for the purchase using a cost segregation. If you were just to purchase the property outright with no leverage, you would be at about 20% of the entire cost of the building,” explains Joe.

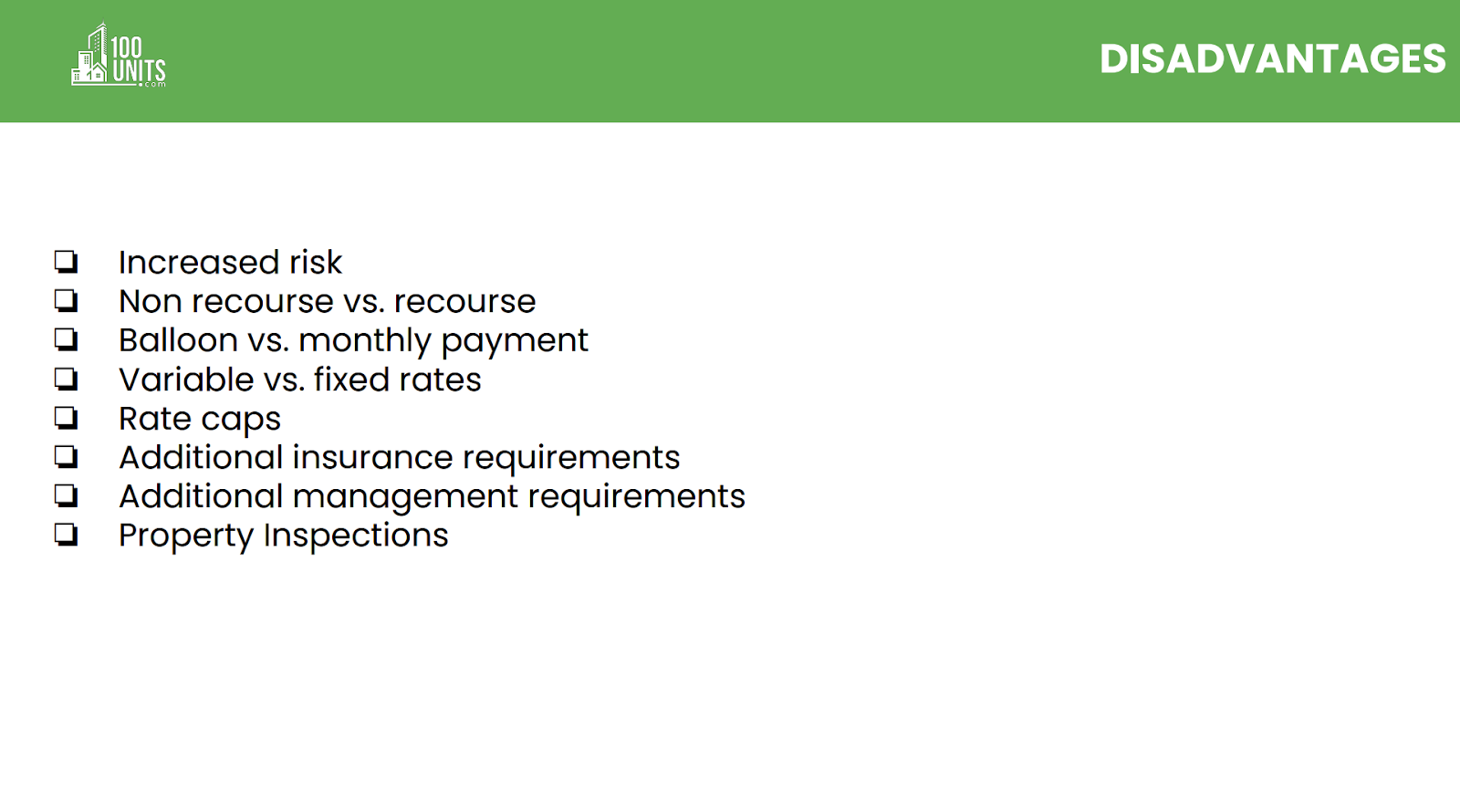

Disadvantages of using leverage

Joe goes into detail on the disadvantages of using leverage for multifamily financing. He speaks on the importance of knowing the difference between non-recourse and recourse, variable rates and interest rates, and how these aspects can affect your financial decisions.

“100% of foreclosed properties had mortgages. So there is increased risk when you take on leverage and that is just part of the business of using leveraged assets. One of the major things to know the difference is between non-recourse and recourse debt.”

Q & A

At the end of his presentation, Joe opened the floor to answer attendees’ questions. We compiled the highlights of Joe’s answers from the Q&A below that we believe would benefit anyone needing advice or tips on multifamily financing.

Q: It’s a broad question, but what are you seeing for foreign buyers getting financing? Specifically Canadians?

A: Canadians are our friendly neighbors to the north, and we have a very good relationship. There are quite a number of lending institutions. To give you an idea, you have RBC and TD Bank, both Canadian banks that operate here, so they’re the easiest to talk to. There are also several other credit unions and banks that will lend readily to Canadians. Then you have the distinction between a complete foreign national with no Green Card, no status here at all, or someone who has some type of status and is just not a citizen.

For someone with no immigration status here looking for a loan, typically, you’ll max out at about 50% loan to value. Now, there are some in the portfolio lending space that I’ve seen push up to 70% loan to value for foreign nationals with zero, no Social Security number, no anything, no tax return, no nothing in the United States. And that’s a space for portfolio lenders. Their interest rate will be a little higher, but it’s something to know that it does exist.

You can watch the virtual event in full here.

We would like to thank all our attendees for joining us for our Connect & Invest multifamily financing event. We appreciate everyone’s participation, and we hope you found these insights and tips helpful in preparing you for your next multifamily investment.

Looking for an experienced Orlando, Tampa, or Jacksonville multifamily broker?

We’re ready to help! Browse our selection of available multifamily properties or contact us today.