Analysis of new multifamily and real estate reports from CBRE & PwC

What’s in store for the multifamily market as we head towards 2021?

As the COVID-19 pandemic continues, there’s plenty of uncertainty in the air. However, the latest multifamily reports show several indications of resilience, renewed investment, and rebound in the coming months.

Read our previous roundup:

Road to recovery: Tracking the positive signs for the multifamily market

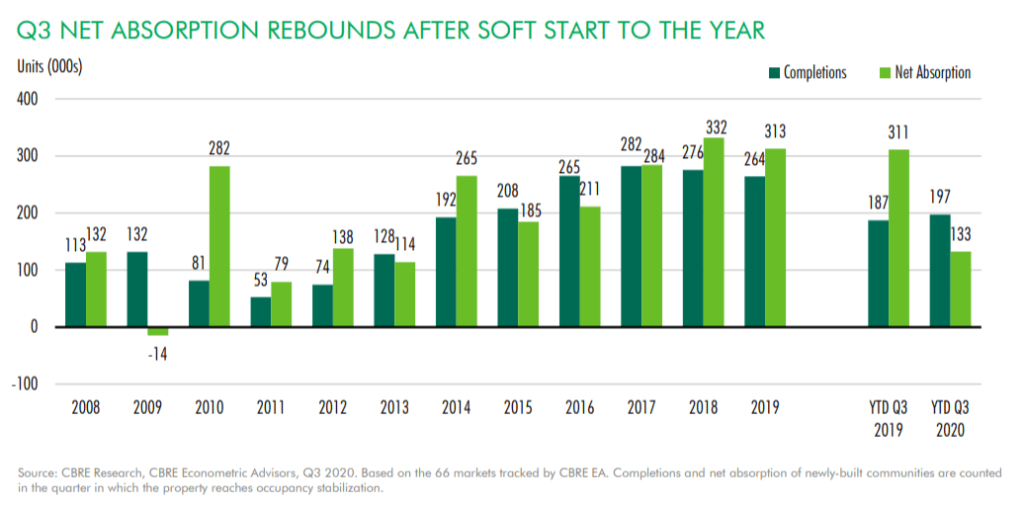

Net absorption outpaces completions

In CBRE’s newly published “U.S. Multifamily Figures Q3 2020” report, we see that net absorption jumped by 300% quarter-over-quarter to 90,300 units in Q3. [1]

The Q3 total was down by 27.6% year-over-year, but shows a marked improvement from a particularly weak Q2—which was hampered by the pandemic and a struggling U.S. economy.

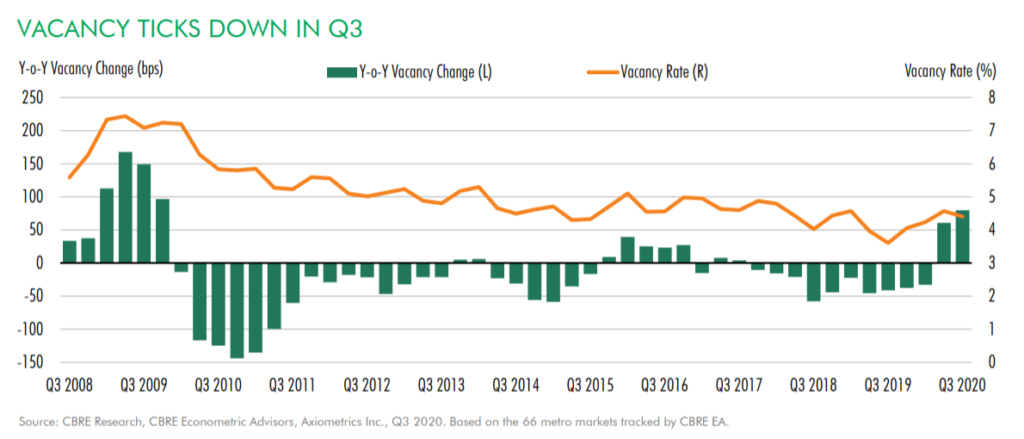

A slight decrease in vacancy rates

The overall vacancy rate edged down 16 basis points (bps) quarter-over-quarter to 4.4%, according to CBRE’s multifamily report.

Despite declining rents—where the average monthly rent fell by 1.6% to $1,694—the multifamily market held up better than expected in Q3 given that enhanced unemployment benefits were not renewed.

CBRE research projects that the multifamily market will stabilize in Q1 2021, with solid recovery throughout the year. Vacancy levels are anticipated to return to pre-pandemic rates by late next year.

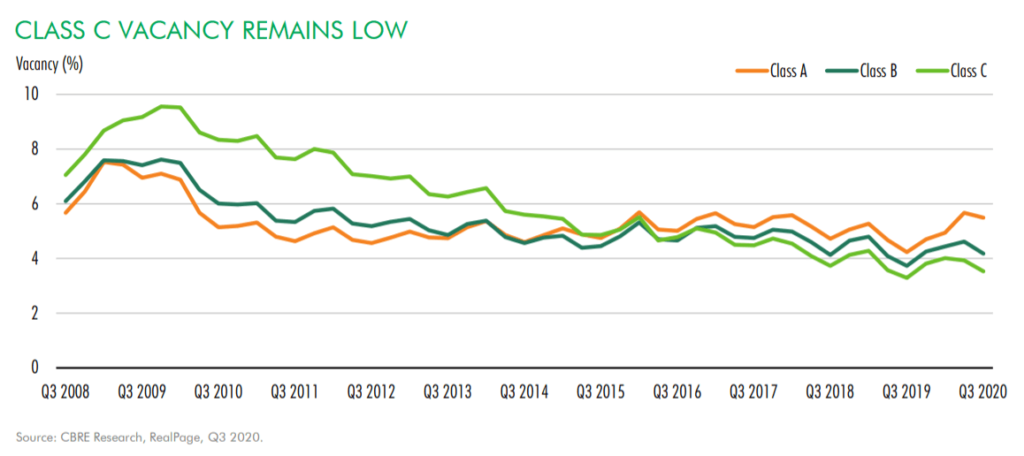

Class B and Class C properties are faring better

Class A properties have felt the most impact from the market downturn, with a smaller decline in vacancy rate compared to Class B and Class C properties.

Class C properties also had the smallest decline in effective rents, and eviction moratoriums have helped to keep renters in place.

CBRE notes that, due to COVID-19, suburban submarkets continued to outperform urban submarkets in Q3. This is also reflected in PwC’s new “Emerging Trends in Real Estate® 2021” report, which states:

“COVID-19 is accelerating suburban growth, especially in the Sunbelt markets. With a greater emphasis on health and safety, the need for lower density environments and more space has only grown. Remote work and higher taxes in large cities due to declining tourism and business tax revenue are contributing to the shift away from an urban core.” [2]

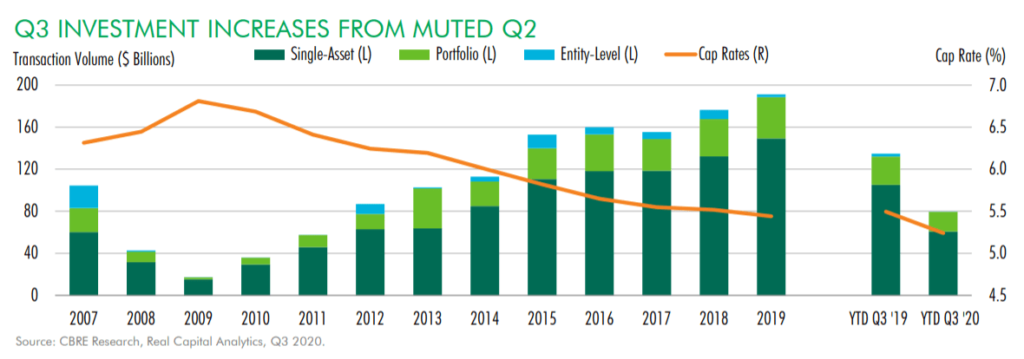

Transactions are bouncing back

Q3 multifamily investment rose by 55.9% quarter-over-quarter to $24.0 billion, following Q2’s lowest quarterly level in almost a decade.

Low interest rates and adequate debt capital were key attracting factors for Q3 buyers, and CBRE expects higher multifamily investment volume in Q4 as investors shift away from poorer-performing property sectors.

What’s next for multifamily?

The pandemic continues to cast a shadow of uncertainty, but these reports show many positive signs for the multifamily market.

“This overall strengthening of multifamily fundamentals is very encouraging to see,” says Joe LaFleur, multifamily investment advisor at 100Units.com. “Locally, we’re definitely noticing renewed investment as the Sunbelt market continues to generate increased interest. As always, we’re following the market closely, and these multifamily reports are promising as we head into 2021 and beyond.”

You can find more insights from Joe here: Expert Viewpoint: The current state of the Central Florida multifamily market.

Stay informed

Visit the rest of our blog for commercial real estate news, investor advice, videos, and more. You can also follow us on Facebook and LinkedIn.

Are you thinking of buying or selling a Central Florida multifamily investment?

We’re ready to help! Browse our selection of available properties or contact us today.

Sources: